How I Protected My Family’s Future Without Betting on Returns

When my kid started high school, I realized saving for college wasn’t enough—what if something happened to our finances before they even graduated? I’d been focused on growth, but ignored the risks hiding in plain sight. After a close call with unexpected medical bills, I shifted my mindset: protecting what we had became just as important as growing it. This is how I rebuilt our plan to safeguard high school education costs—without gambling on markets or promises. It wasn’t about chasing high returns or complex strategies. It was about making sure that no matter what life threw our way, our child’s education stayed on track. That meant rethinking every assumption I’d made about saving, investing, and preparing for the future.

The Wake-Up Call: When Life Interrupted the Plan

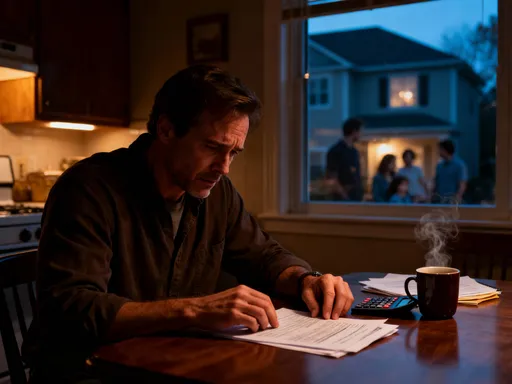

For years, I believed we were doing everything right. We had a dedicated college fund, contributed regularly, and kept a modest emergency account. Our budget wasn’t luxurious, but it worked. Then, during my son’s sophomore year, I had a sudden health issue that required surgery and several weeks off work. The medical bills weren’t fully covered, and even with insurance, we faced thousands in out-of-pocket costs. We dipped into our emergency savings—then kept dipping. Within two months, half of it was gone. That moment changed everything. I realized that while we were saving for the future, we weren’t protected from the present. Our education fund suddenly felt fragile, exposed to any further setbacks. It wasn’t a market crash or economic downturn that threatened our goals—it was everyday life. And that’s when I understood: financial resilience isn’t built just by saving more—it’s built by preparing for what could go wrong.

This experience forced me to confront a truth many parents avoid: having a savings account doesn’t mean you’re secure. Traditional advice often focuses on how much to save, but rarely on how to protect it. A car accident, job loss, or family illness can derail years of disciplined saving in a matter of weeks. For families funding high school and preparing for college, the timing couldn’t be worse. These are not distant concerns—they’re real, recurring risks. According to data from the Federal Reserve, nearly 40% of Americans wouldn’t be able to cover a $400 emergency with cash. That means millions of families are one unexpected expense away from dipping into education funds. I was almost one of them. The wake-up call wasn’t just about money—it was about mindset. I stopped seeing risk as something abstract and started treating it as a central part of planning.

What made this moment so pivotal was the realization that risk isn’t just financial—it’s emotional and psychological too. The stress of not knowing if we could cover basic expenses made it harder to think clearly about long-term goals. I began to see that protecting our financial foundation wasn’t a distraction from saving for college—it was the foundation of it. Without stability, growth means nothing. That shift in perspective led me to redesign our entire approach, not by chasing higher returns, but by building stronger safeguards. The goal was no longer just to accumulate funds, but to ensure they would be there when we needed them most—regardless of what life might bring.

What Risk Management Really Means for Education Funding

When most people think about funding education, their minds jump to investing—529 plans, index funds, stock portfolios. But I learned that before you can grow money safely, you have to understand what could shrink it. Risk management isn’t about avoiding all risk; it’s about identifying which risks are most likely to affect your family and planning for them intentionally. For us, the biggest threats weren’t market swings—they were job instability, health issues, and unexpected expenses that could force us to pull from education savings. These are not rare events. A study by the U.S. Bureau of Labor Statistics shows that workers hold an average of 12 jobs in their lifetime, and many experience involuntary job changes. Meanwhile, medical costs remain one of the leading causes of financial strain, even for insured families.

So I started asking different questions. Instead of “How can I earn 7% annually?” I asked, “What would happen if my income dropped by 30% for six months?” or “Could we still afford senior year activities if I had another medical emergency?” These weren’t hypotheticals—they were plausible scenarios. I realized that focusing only on returns was like building a house and forgetting the foundation. The roof might look impressive, but if the ground shifts, everything collapses. Risk management means accepting that uncertainty is part of life and designing a plan that can absorb shocks without derailing long-term goals.

One of the most valuable lessons was learning to distinguish between systemic risks and personal risks. Systemic risks—like recessions or inflation—affect everyone and are harder to control. Personal risks—like illness, job loss, or car repairs—are specific to your household but often more predictable and manageable. I couldn’t control the stock market, but I could control whether we had disability coverage or a three-month cash buffer. By focusing on what I could influence, I reduced anxiety and increased confidence. This isn’t about fear-mongering—it’s about clarity. Knowing which risks matter most allowed me to allocate resources wisely, rather than reacting in crisis mode. For education funding, that meant prioritizing stability over speculation, and protection over performance.

Separating the Essentials from the Optional: A New Budget Mindset

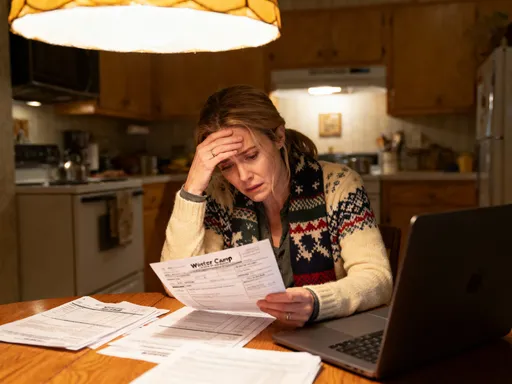

After the medical incident, I went back to our household budget with fresh eyes. I wasn’t looking to cut out all luxuries—life should still have joy—but I needed to know what was essential and what could flex. I created a new category: non-negotiable priorities. At the top was education. Whether it was AP exam fees, SAT prep courses, or senior trip costs, these were expenses we would protect at all costs. Everything else—dining out, streaming subscriptions, seasonal decor—became variable. This wasn’t austerity; it was intentionality. I realized that many families save what’s left over, but I decided to spend what’s left after saving. That small shift changed everything.

I broke our spending into three layers: fixed essentials (housing, utilities, groceries), protected goals (education, retirement), and flexible lifestyle items. Each month, the first transfers went to the protected goals. Only after those were funded did we allocate money to the flexible category. If something unexpected came up, we adjusted the flexible spending—not the essentials. This gave us breathing room without compromising what mattered. For example, we paused our weekend takeout budget for two months to replenish part of the emergency fund. It wasn’t painful; it was empowering. We were making conscious choices, not reacting to shortages.

This approach also helped me see where money was leaking. I discovered we were paying for services we rarely used—gym memberships, unused software subscriptions, and duplicate insurance coverage. By canceling just three of these, we freed up nearly $150 a month. That didn’t go to more spending—it went into a dedicated education reserve. Over two years, that small change added over $3,600 to our college fund, all without increasing income. The lesson was clear: budgeting isn’t about restriction—it’s about alignment. When your spending reflects your true priorities, every dollar works harder. And when education is treated as a non-negotiable, it stops being vulnerable to life’s surprises.

Building a Safety Net That Works Before the Crisis Hits

For years, I viewed insurance as just another monthly bill—an unavoidable cost with no immediate benefit. That changed when I reviewed our coverage after the hospital visit. I discovered that our health plan had high deductibles and didn’t cover certain rehab services. But because we had a supplemental disability policy I’d almost canceled as “too expensive,” a portion of my income was replaced during recovery. That wasn’t luck—it was planning. I began to see protection tools not as expenses, but as financial shock absorbers. Just like seatbelts don’t prevent accidents but reduce harm, these tools don’t stop crises—but they keep them from becoming catastrophes.

I started building layers of protection. First, I increased our emergency fund to cover six months of essential expenses—not everything, just what we absolutely needed to survive. This wasn’t meant to fund vacations or upgrades—just to keep the lights on and the roof over our heads during a crisis. Next, I reviewed life and disability insurance. I opted for a low-cost term life policy that would cover college costs if something happened to me. It wasn’t about replacing my full income—just ensuring our child could finish school without financial burden. Disability insurance, often overlooked, became a priority because it protects earning ability—the real engine of family finances.

I also explored umbrella liability coverage, a low-cost policy that protects against lawsuits. While it felt remote, I realized that one accident—like a visitor getting injured at home—could lead to legal costs that drain savings. For less than $200 a year, we gained an extra $1 million in coverage. These tools aren’t glamorous, but they’re effective. They form a protection stack that works silently in the background. The key was avoiding over-insurance—buying only what we needed based on real risks, not fear. By treating protection as infrastructure, like plumbing or electricity, I stopped seeing it as optional. Just as you wouldn’t skip home repairs until the roof leaks, you shouldn’t wait for a crisis to build your safety net.

Smarter Saving: Where to Keep the Money Without Chasing Returns

I used to believe that to grow money, I had to take on risk. I opened a brokerage account, invested in index funds, and watched the balance fluctuate. Some months were great; others, I lost sleep. When I needed to pay for a summer program, I had to withdraw during a dip. That’s when I realized: chasing returns can cost you more than low returns ever could. I shifted my strategy to focus on cash flow alignment—matching when I’d need the money with how I saved it. For expenses due in one to three years, I moved funds into stable, accessible accounts.

I explored several low-volatility options. High-yield savings accounts offered better interest than traditional banks, with full liquidity. I used these for near-term costs like application fees and dorm supplies. For expenses two to four years out, I looked at short-term certificates of deposit (CDs) and Treasury securities. These provided slightly higher returns with minimal risk, and I staggered the maturity dates so money would be available when needed. I also considered I-bonds, which are inflation-protected savings bonds issued by the U.S. Treasury. While they have holding period rules, they offered a way to preserve purchasing power without market exposure.

The biggest change was letting go of the need to “beat the market.” I stopped comparing my savings rate to stock performance. Instead, I measured success by stability and access. If my high-yield account earned 4% while the S&P returned 10%, I didn’t feel behind. I felt secure. Because I knew that when senior year tuition was due, the money would be there—intact, available, and stress-free. This approach isn’t about maximizing growth; it’s about minimizing regret. It’s choosing peace of mind over potential gain. And for a parent funding education, that trade-off is not only rational—it’s responsible.

Preparing for the Unpredictable: Scenario Planning Made Simple

One of the most powerful tools I adopted was scenario planning—running simple “what-if” exercises to test our financial resilience. I didn’t need complex software or financial modeling. I used a spreadsheet and asked honest questions: What if my income dropped by 30% for six months? What if college costs rose faster than expected? What if we faced another medical emergency? For each scenario, I mapped out our available resources, potential cuts, and fallback options. This wasn’t about predicting the future—it was about reducing panic when surprises happen.

For example, I modeled a job loss scenario. I listed all income sources, then removed my salary. I checked how long our emergency fund would last, which bills could be paused (like subscriptions), and which protections would kick in (like unemployment or disability). I also identified quick-access assets—like a small cash reserve in a money market account—that could cover essentials without touching education savings. Knowing these steps in advance removed the fear of the unknown. It turned a potential crisis into a manageable situation with a clear action plan.

I also projected tuition increases. College costs have historically risen faster than inflation. I built a conservative estimate—5% annual increase—and recalculated our savings target. This showed a gap, so I adjusted by increasing monthly contributions slightly and redirecting some flexible spending. The exercise didn’t guarantee we’d cover every possible increase, but it ensured we weren’t blind to it. Scenario planning gave me confidence that we weren’t just hoping for the best—we were prepared for more than the best. It transformed financial planning from a passive activity into an active defense strategy.

Putting It All Together: A Balanced, Real-World Approach

Today, our financial plan isn’t about hitting aggressive return targets or outsmarting the market. It’s about staying on course—consistently, calmly, and confidently. I’ve learned that protecting your family’s future doesn’t require complex strategies or risky bets. It requires clarity, discipline, and a willingness to prepare for what could go wrong. Our approach balances growth with guardrails: we still invest for long-term goals, but we do it with a foundation of protection. Education savings are shielded in stable accounts, emergencies are funded, and risks are managed through intentional choices.

The pieces fit together like a puzzle. Budgeting clarifies priorities. Protection absorbs shocks. Stable saving preserves value. Scenario planning builds readiness. None of it is flashy, but each part strengthens the whole. I no longer lie awake worrying about market drops or unexpected bills. Not because risks have disappeared—but because we’ve built a system that can handle them. That peace of mind is priceless. More than any return, more than any balance sheet, it’s the real measure of financial success.

To other parents navigating the high school years, I’d say this: don’t wait for a crisis to rethink your plan. Start today. Identify your non-negotiables. Build your safety net. Align your savings with your timeline. You don’t need to be rich to be resilient. You just need to be thoughtful. Protecting your family’s future isn’t about avoiding risk altogether—it’s about managing it wisely. And when your child walks across the stage at graduation, knowing you kept your promises without sacrificing security—that’s the greatest return of all.